Introduction

Many traders spend endless hours debating win rate vs. risk-to-reward (R:R) ratios. While those are important, the missing piece of the puzzle is often position sizing. Without consistent and proper position sizing, even the most mathematically sound win rate and R:R setups can crumble.

In this blog, we’ll break down how position sizing impacts profitability, explore different methods, and walk through practical tools and strategies for managing risk effectively.

Why Position Sizing Matters

Position sizing ensures that your risk per trade stays consistent. This consistency is what makes win rate and R:R work in your favor.

Consider this example:

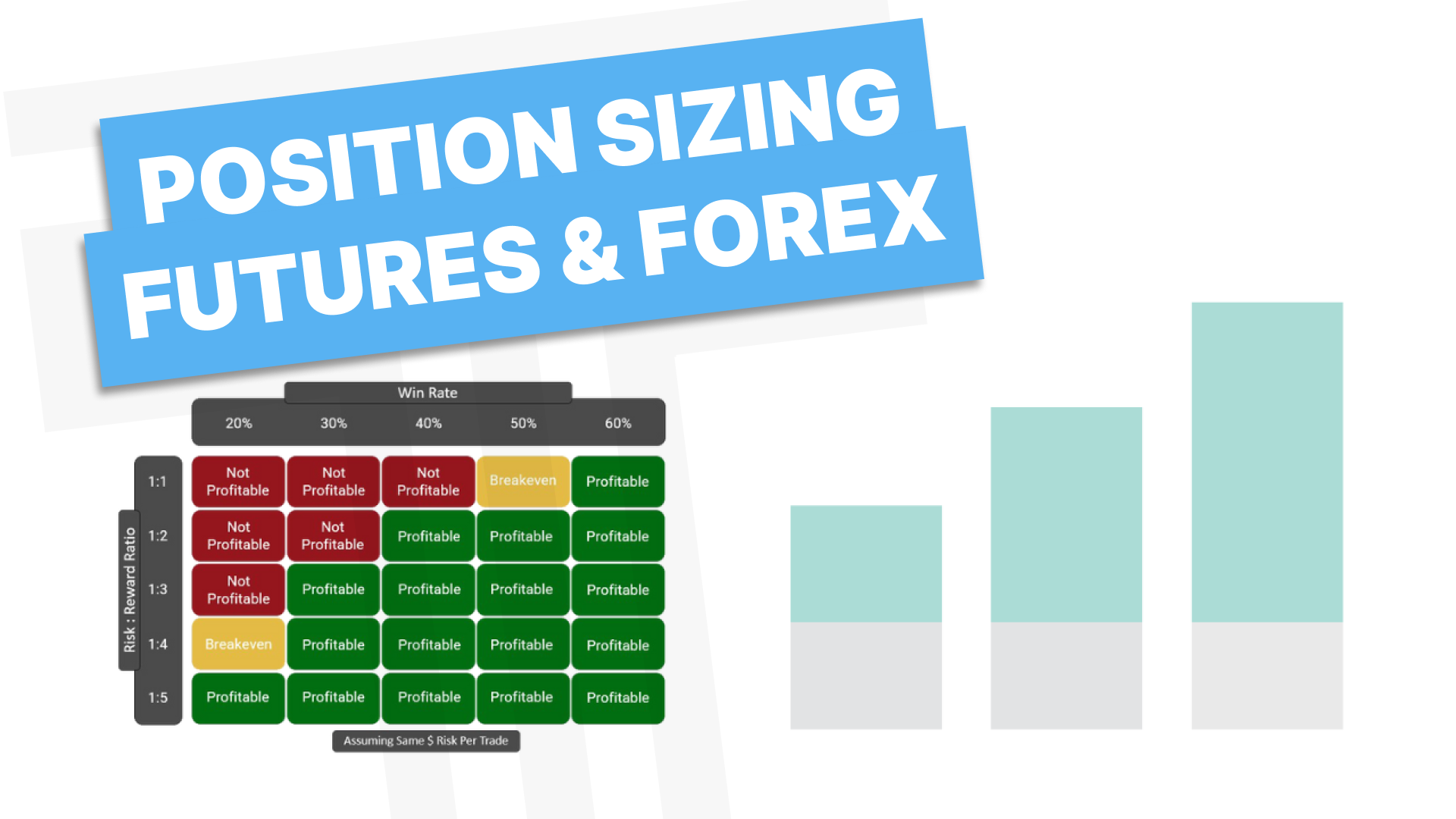

System: 1:2 R:R, 50% win rate

Risk: $1,000 per trade

If you lose the first trade (-$1,000) and win the second (+$2,000), you’re up +$1,000 overall. That’s how the math should work.

But if you lose on the first trade ($1,000 loss) and then cut risk on the second ($500 risk) and it wins (+$1,000 instead of +$2,000), you end up at break-even instead of up (+$1,000). This is why inconsistent sizing undermines trading systems.

Fixed Contract Size vs. Fixed Dollar/Percentage Risk

There are several ways to size positions:

Fixed Contract Size – e.g., always trading 2 NQ contracts.

Problem: Risk fluctuates wildly depending on stop size.

Example: Risk could be $400 on one trade and $1,600 on another, creating inconsistent R values.

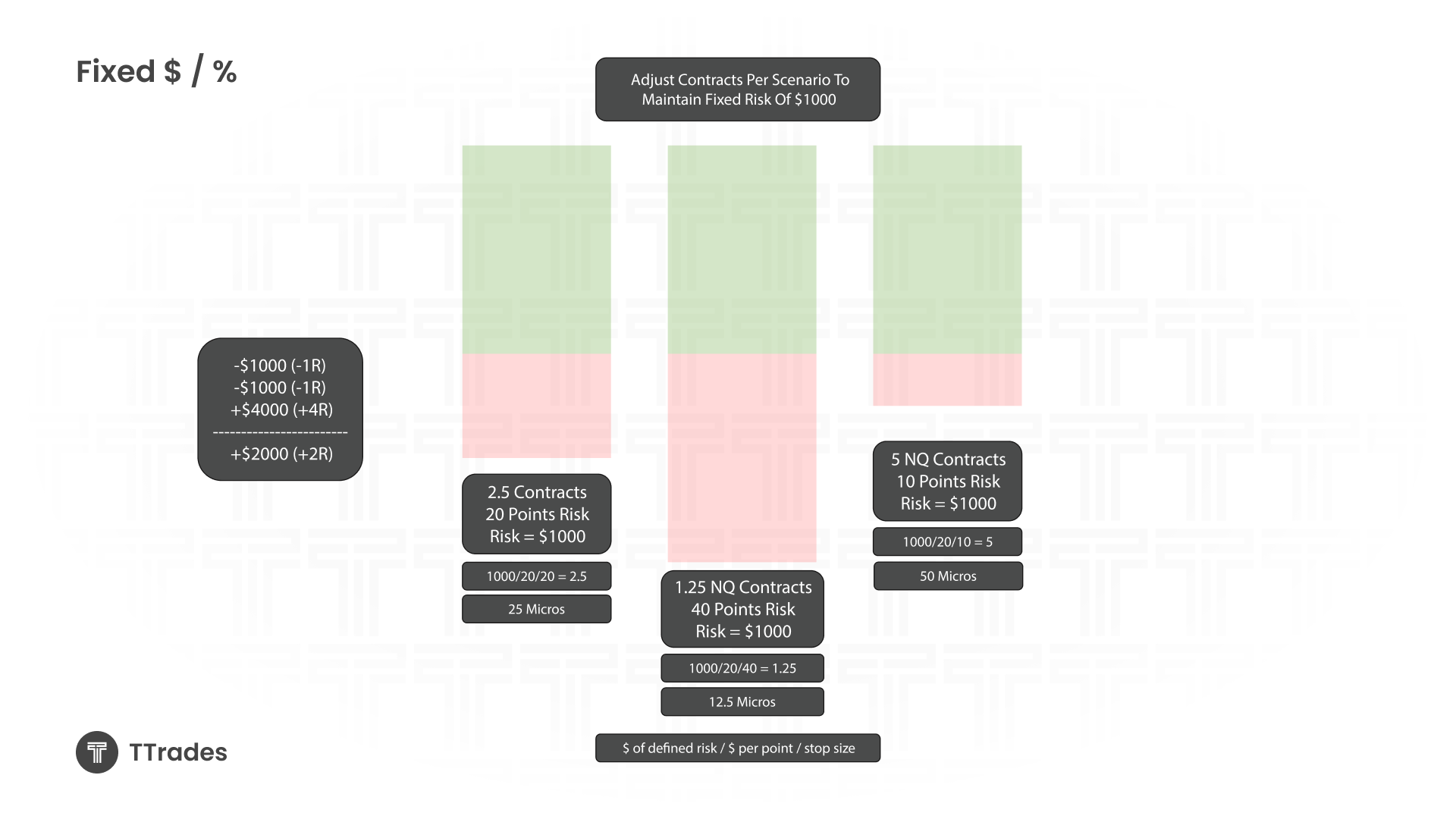

Fixed Dollar or Percentage Risk – e.g., always risking $1,000 or 1% of account per trade.

Advantage: Keeps risk steady across trades, ensuring R:R outcomes remain accurate.

Example: Two losses at -$1,000 each followed by a 4R win, +$4,000 win equals +$2,000 net.

Fixed contract size makes sense if traders always have the same sized stop loss. Due to the fluctuations in market volatility, this is rarely the case.

Calculating Position Size

To determine the correct size, you’ll need three inputs:

Defined risk per trade (e.g., $1,000)

Value per point (instrument specific, e.g., NQ = $20/point)

Stop size (in points/pips)

Formula:

Contracts = (Risk $) ÷ (Value per point × Stop size)

For example:

Risk = $1,000

NQ Value = $20/point

Stop = 20 points

$1,000 ÷ (20 × 20) = 2.5 contracts

Since you can’t trade half contracts on futures, using micros allows greater flexibility.

Tools for Position Sizing

Manually calculating every trade is time-consuming. Thankfully, there are simple tools to make this process easier:

Spreadsheets/Calculators – Input account size, desired risk, and stop size to instantly get contract or lot size.

TradingView Risk-Reward Tool – Lets you set entry, stop, and account risk %, then automatically calculates quantity.

Prop Firm Accounts and Position Sizing

Prop firm accounts add a twist. While you may “have” a $25,000 account, the real limiting factor is the drawdown (e.g., $1,500).

Risking 1% of the account ($250) may actually equal ~17% of drawdown.

This drastically increases the chance of blowing the account after just a few losses.

Instead, consider a risk of 7–10% of drawdown per trade, which typically allows 10–15 consecutive losing trades before the account is gone. Once funded, reducing risk further creates more breathing room.

Key Takeaways

Consistent position sizing is the foundation of trading.

Decide between fixed contract and fixed $ risk. (micros help!)

Use spreadsheets, or tools on TradingView to size positions correctly.

For prop firm accounts, always size based off the drawdown amount, not account balance.

Position sizing isn’t glamorous, but it’s what keeps traders alive long enough to let their strategies work. Master it, and your win rate and R:R finally have a chance to work out.